Roth IRA Withdrawal Guide

Understand the rules, timelines, and penalties for withdrawing from your Roth IRA. Make informed decisions about your retirement savings.

The Fundamental Distinction

Understanding the difference between contributions and earnings is key to maximizing your Roth IRA benefits.

The money you directly contribute to your Roth IRA can be withdrawn at any time, for any reason, completely tax-free and penalty-free.

Key Benefit: Your principal is always accessible, offering flexibility and peace of mind.

The profits from your investments (interest, dividends, capital gains) are subject to specific rules to be withdrawn tax-free and penalty-free.

Important: Earnings require meeting the 5-year rule and a qualifying event.

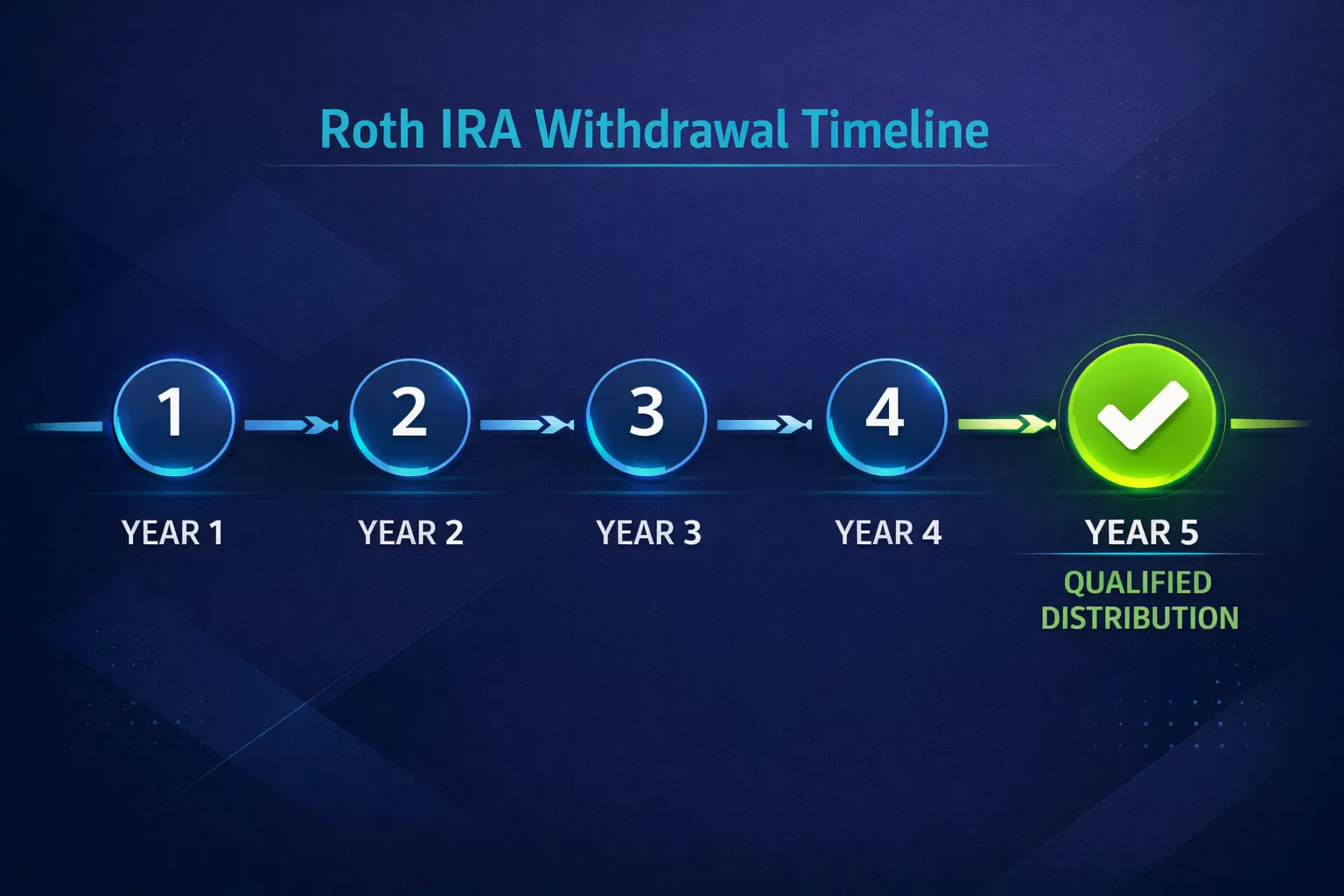

The Five-Year Rule

Your Roth IRA must be established for at least 5 years before earnings can be withdrawn tax-free and penalty-free.

The five-year period begins on January 1st of the tax year for which you made your first contribution to any Roth IRA.

Example: If you contribute in April 2026 for the 2025 tax year, the clock starts January 1, 2025.

Roth conversions have a separate five-year rule for each conversion. Withdrawing converted amounts before the period ends may trigger a 10% penalty.

Exceptions apply for disability, death, and age 59½.

Qualified Distribution Requirements

To withdraw earnings tax-free and penalty-free, two conditions must be met.

This rule applies to the Roth IRA account itself, not to individual contributions. Once your first Roth IRA is opened, the five-year clock starts for all Roth IRAs you own.

Note: This is a universal rule across all your Roth IRAs. Opening a second Roth IRA does not restart the clock.

Withdrawal Ordering Rules

The IRS has specific rules about which funds are withdrawn first. This determines the tax and penalty consequences.

Regular Contributions

Always withdrawn first and are both tax-free and penalty-free, regardless of timing or age.

Converted and Rollover Amounts

Distributed after regular contributions. May be subject to a 10% penalty if withdrawn before the specific five-year period for that conversion is met.

Earnings

Distributed last. If withdrawn as part of a non-qualified distribution, subject to both ordinary income tax and a 10% early withdrawal penalty.

Non-Qualified Withdrawals: Penalties & Taxes

If you withdraw earnings before meeting both the five-year rule and a qualifying event, you'll face taxes and penalties.

The earnings portion of your withdrawal will be taxed at your regular income tax rate.

An additional 10% penalty will be applied to the earnings portion of the withdrawal.

Example Scenario

You withdraw $5,000 from your Roth IRA after 3 years, consisting of $3,000 in contributions and $2,000 in earnings. You're 45 years old.

- ✓Contributions ($3,000): Withdrawn tax-free and penalty-free

- ✗Earnings ($2,000): Subject to ordinary income tax + 10% penalty ($200)

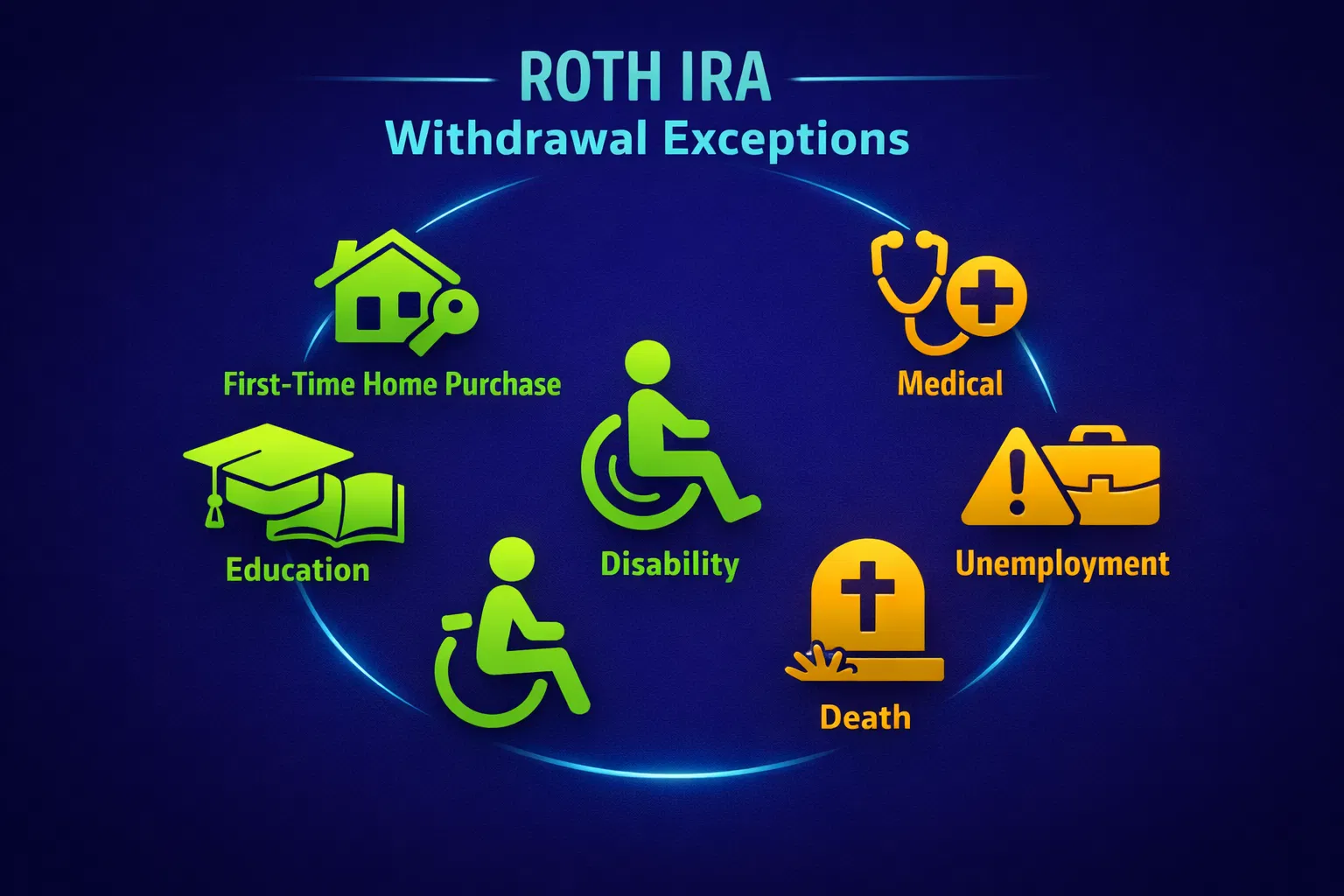

Exceptions to the 10% Penalty

Even if you're under 59½ and the distribution is non-qualified, certain situations may allow you to avoid the 10% penalty.

Up to $10,000 lifetime limit

Tuition, fees, books, and room & board

Exceeding a certain % of AGI

While unemployed

Totally and permanently disabled

Distributions to beneficiaries

Important Note: Even if an exception applies and you avoid the 10% penalty, you may still owe ordinary income tax on the earnings portion of your withdrawal. Consult with a tax professional to understand your specific situation.

Calculate Your Withdrawal Impact

Use this interactive calculator to estimate taxes and penalties for your specific withdrawal scenario. Adjust the inputs to see how different factors affect your net withdrawal amount.

$1,000 - $100,000

Contributions: $3,000 | Earnings: $2,000

✗ Five-year rule NOT met (2 years remaining)

✗ Under age 59½

2025 tax brackets (single filer). Adjust based on your filing status.

Select if you qualify for an exception to the 10% penalty

Five-Year Rule: NOT MET ✗

Age 59½+: NO ✗

Qualified Distribution: NO ✗

Estimated Breakdown

$3,000

Tax-free & penalty-free

$2,000

Subject to conditions

$440

22% bracket

$200

On earnings only

Total Taxes & Penalties

$640

12.8% of withdrawal amount

Amount You Receive

$4,360

After all taxes and penalties

Disclaimer: This calculator provides estimates based on 2025 tax brackets and is for educational purposes only. Actual taxes and penalties may vary based on your specific tax situation, filing status, state taxes, and other factors. Consult with a qualified tax professional for accurate calculations.

Save different withdrawal scenarios to compare them side-by-side

Download Your Reference Guide

Get a one-page PDF summary of key withdrawal rules and exceptions that you can print, save, or share with your clients.

Roth IRA Quick Reference

A comprehensive one-page guide covering withdrawal rules, the five-year rule, qualified distributions, penalties, and exceptions.

- All key withdrawal rules

- Penalty information

- Exception scenarios

- Easy reference tables

Ready to Make Informed Decisions?

Consult with a tax or financial advisor to discuss your specific Roth IRA withdrawal strategy and ensure compliance with all regulations.